In financial markets, startups have often attempted to brand themselves as “tech firms” in hopes of being valued using tech-company multiples, and frequently, they achieve this — at least temporarily.

Traditional institutions have learned this lesson the hard way. Throughout the 2010s, many companies scrambled to redefine themselves as technology firms. Banks, payment processors, and retailers began referring to themselves as fintechs or data firms. However, few actually managed to achieve the valuation multiples of true tech companies because the fundamentals rarely aligned with the narrative.

WeWork stands as one of the most notorious examples: a real estate company masquerading as a tech platform that ultimately collapsed under the burden of its own facade. In financial services, Goldman Sachs launched Marcus in 2016 as a digital-first platform to compete with consumer fintechs. Despite initial success, the initiative was scaled back in 2023 due to ongoing profitability challenges.

JPMorgan famously declared itself “a technology company with a banking license,” while BBVA and Wells Fargo invested heavily in digital transformation. Nonetheless, few of these efforts yielded platform-level economics. Today, there exists a graveyard of corporate tech illusions — a stark reminder that no branding can transcend the structural limitations of capital-intensive or regulated business models.

Crypto is now facing a similar identity crisis. DeFi protocols aspire to be valued like Layer 1s, while real-world asset (RWA) dApps present themselves as sovereign networks. Everyone is in pursuit of the Layer 1 “technology premium.”

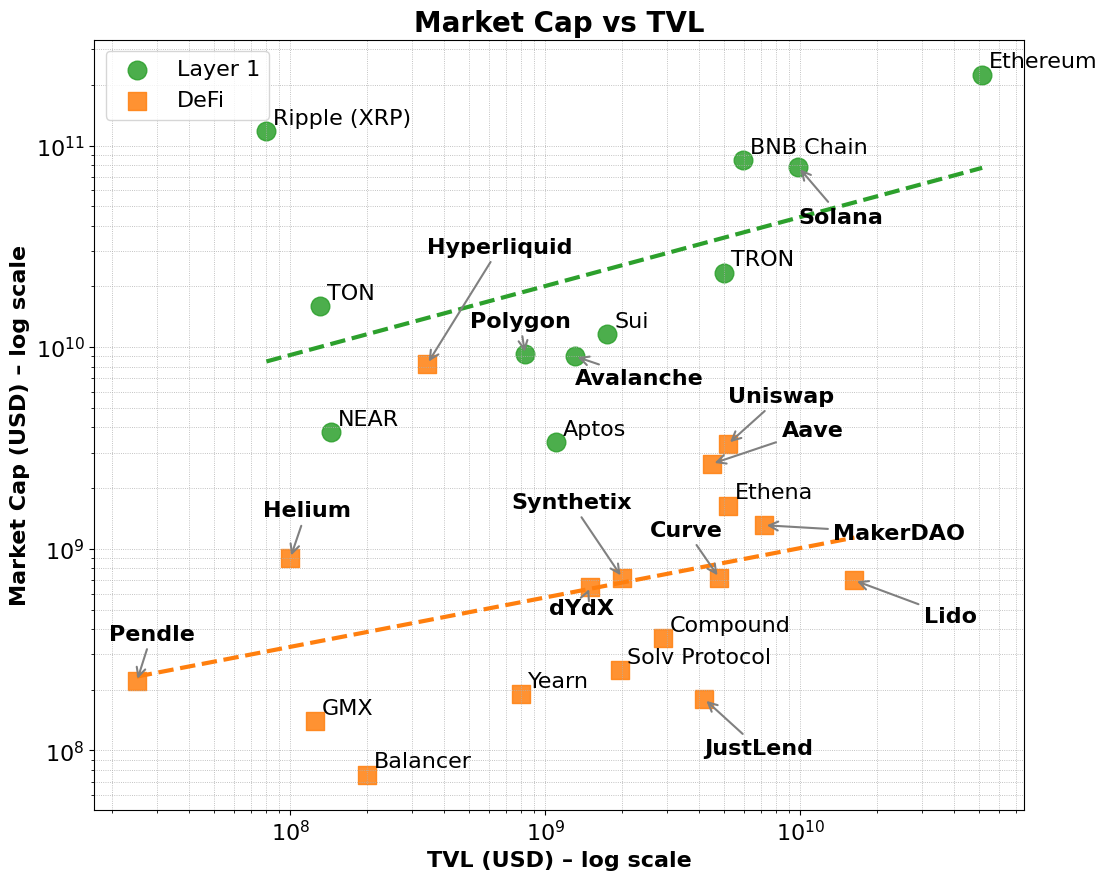

To be fair, that premium is genuine. Layer 1 networks such as Ethereum, Solana, and BNB consistently achieve higher valuation multiples compared to metrics like Total Value Locked (TVL) and fee generation. These networks benefit from a broader market narrative that favors infrastructure over applications and platforms over products.

This premium persists even when fundamentals are factored in. Many DeFi protocols show strong TVL or fee generation but still struggle to reach comparable market capitalizations. In contrast, Layer 1s attract early users through validator incentives and native token economics, then expand into developer ecosystems and composable applications.

Ultimately, this premium reflects Layer 1s’ ability to provide broad native token utility, ecosystem coordination, and long-term extensibility. Additionally, as fee volume increases, these networks often experience disproportionate rises in market capitalization — indicating that investors are factoring in not just present use, but future potential and compounding network effects.

This layered flywheel, moving from infrastructure adoption to ecosystem growth, illustrates why Layer 1s consistently garner higher valuations than dApps, even when performance metrics appear similar.

This parallels how equity markets differentiate platforms from products. Infrastructure companies like AWS, Microsoft Azure, Apple’s App Store, or Meta’s developer ecosystem go beyond being service providers — they are ecosystems. They enable countless developers and businesses to build, scale, and interact. Investors assign higher multiples not merely for current revenues, but for the potential to support emerging use cases, network effects, and economies of scale. Conversely, even highly profitable SaaS tools or niche services rarely attract the same valuation premium, as their growth is limited by restricted API composability and narrow utility.

A similar trend is emerging among large language model (LLM) providers. Most are hastening to brand themselves not as chatbots, but as foundational infrastructure for AI applications. Everyone wants to be AWS — not Mailchimp.

Layer 1s in crypto embody this logic as well. They’re not merely blockchains; they serve as coordination layers for decentralized computation and state synchronization. They support a wide array of composable applications and assets. Their native tokens gain value through base-layer activities: gas fees, staking, MEV, and more. Crucially, these tokens also function as mechanisms to incentivize developers and users. Layer 1s benefit from self-reinforcing loops between users, builders, liquidity, and token demand, supporting both vertical and horizontal scaling across sectors.

In contrast, most protocols are not real infrastructure. They are single-purpose products. Thus, adding a validator set does not transform them into Layer 1s; it merely adorns a product with infrastructure optics to justify a higher valuation.

This brings us to the appchain trend. Appchains integrate application, protocol logic, and a settlement layer into a vertically cohesive stack. They promise improved fee capture, user experience, and “sovereignty.” In some cases — like Hyperliquid — they deliver. By controlling the entire stack, Hyperliquid has achieved rapid execution, outstanding UX, and significant fee generation — all without relying on token incentives. Developers can also deploy dApps on its underlying Layer 1, taking advantage of its high-performance decentralized exchange infrastructure. Although its scope remains limited, it hints at broader scaling potential.

However, most appchains are merely protocols attempting to rebrand, lacking substantial usage and ecosystem depth. They are engaged in a two-front battle: trying to develop both infrastructure and a product at once, often without the necessary capital or team to excel in either. The result is a blurry hybrid — neither a robust Layer 1 nor a category-defining dApp.

This scenario is familiar. A robo-advisor with an appealing interface is still a wealth manager. A bank with open APIs remains a balance-sheet business. A coworking company with a polished app continues to merely rent office space. Eventually, the hype fades — and the market adjusts accordingly.

RWA protocols now find themselves falling into the same trap. Many are marketing themselves as infrastructure for tokenized finance — but without meaningful differentiation from existing Layer 1s, or sustainable user adoption. At best, they represent vertically integrated products with no compelling necessity for a sovereign settlement layer. Worse, most haven’t established product-market fit in their primary use case and instead bolt on infrastructure while leaning into inflated narratives to justify valuations unsupported by their economics.

So what’s the way forward?

The answer isn’t to feign infrastructure status. It’s to embrace your role as a product or service — and execute it exceptionally well. If your protocol solves an actual problem and drives meaningful TVL growth, that’s a solid foundation. But TVL alone won’t make you a successful appchain.

What truly matters is genuine economic activity: TVL that leads to sustainable fee generation, user retention, and clear value accumulation for the native token. Moreover, if developers build on your protocol because it’s truly useful — not because it claims to be infrastructure — the market will reward you. Platform status is earned, not self-proclaimed.

Some DeFi protocols — like Maker/Sky and Uniswap — are heading in this direction. They’re evolving towards appchain-style models that enhance scalability and cross-network access. However, they do so from a position of strength: armed with established ecosystems, clear monetization, and product-market fit.

Conversely, the emerging RWA sector has yet to demonstrate lasting traction. Nearly every RWA protocol or centralized service is rushing to launch an appchain — often backed by fragile or untested economics. As with leading DeFi protocols transitioning to an appchain model, the optimal path for RWA protocols is to initially leverage existing Layer 1 ecosystems, build user and developer traction that fosters TVL growth, demonstrate sustainable fee generation, and only then evolve towards an appchain infrastructure model — with a clear purpose and strategy.

Thus, in the case of an appchain, the utility and economics of the foundational application must take precedence. Only once these are established does a transition to a sovereign Layer 1 become feasible. This contrasts with the growth trajectory of general-purpose Layer 1s, which can initially focus on building a validator and trader ecosystem. Early fee generation is driven by native token transactions, and over time, cross-market scaling broadens the network to include developers and end users — ultimately spurring TVL growth and diversified fee streams.

As crypto matures, the haze of storytelling is dissipating, and investors are becoming more discerning. Buzzwords like “appchain” and “Layer 1” no longer capture attention on their own. Without a clearly defined value proposition, sustainable token economics, and a well-articulated strategic direction, protocols lack the foundational elements necessary for any credible transition to genuine infrastructure.

What crypto needs — especially in the RWA space — isn’t more Layer 1s. It needs better products. The market will reward those who focus on precisely that.

Leave a Reply