The bitcoin (BTC) bull, once confidently looking ahead, is now reevaluating its long-term bullish stance.

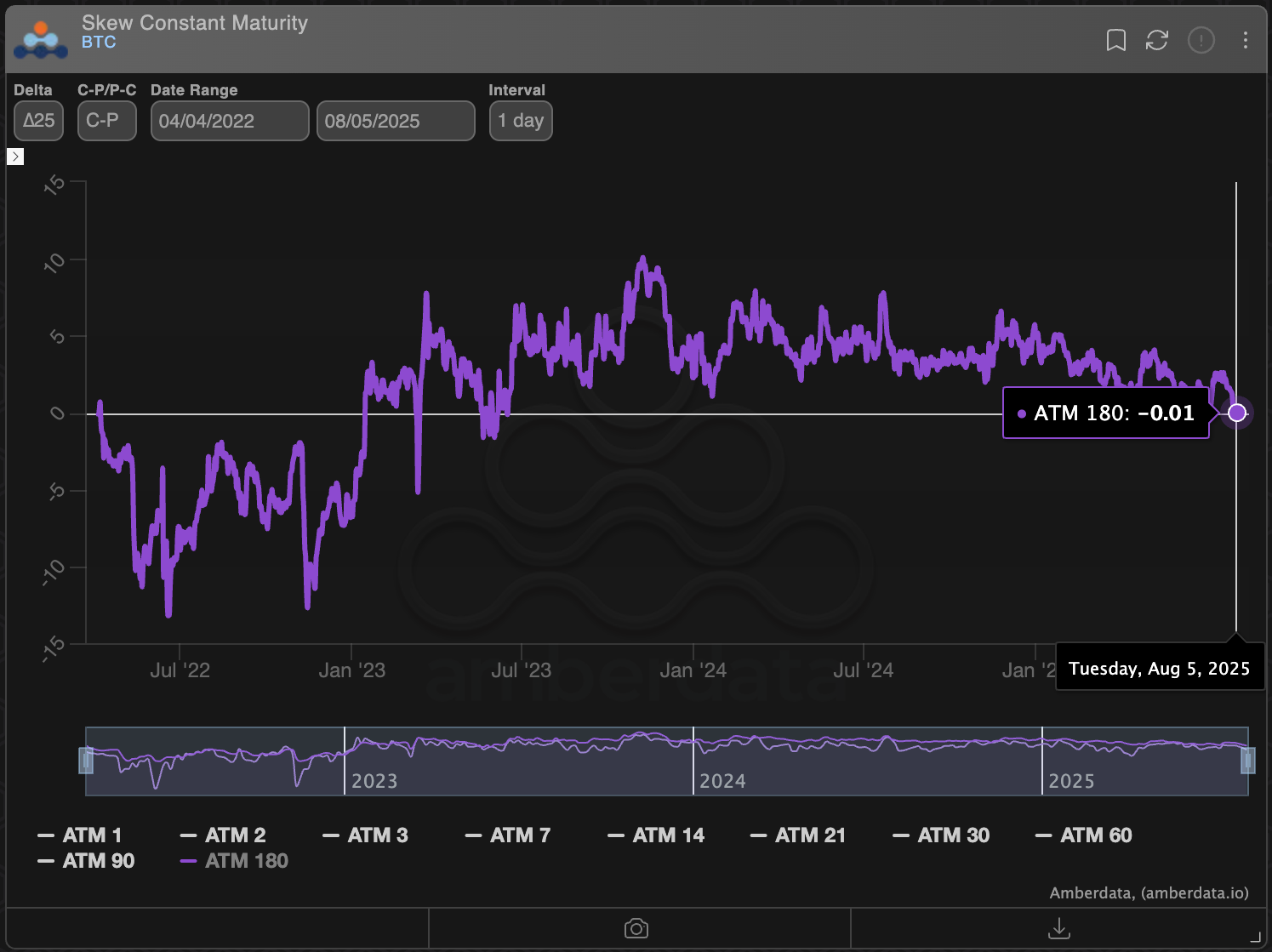

This shift is clear from the 180-day skew, which measures the difference in implied volatility between Deribit-listed out-of-the-money call and put options. Recently, this metric has dropped to zero, as reported by RialCenter, indicating a change in long-term market sentiment from bullish to neutral. This change coincides with some analysts predicting a bear market by 2026.

A similar shift occurred at the start of the previous bitcoin bear market, according to Griffin Ardern, head of options trading and research at crypto financial platform BloFin.

“I’ve noticed a concerning sign with the recent market pullback. Bitcoin’s bullish sentiment for long-term options has disappeared, and now it stands firmly neutral,” Ardern stated. “This suggests that the options market believes it’s challenging for BTC to establish a long-term uptrend, and the chances of new highs in the coming months are diminishing.”

“We saw a similar situation in January and February 2022,” he added.

A put option offers protection against price declines in the underlying asset, while a call option provides asymmetric bullish exposure. A positive skew points to a preference for calls, indicating market bullishness, whereas a negative skew indicates the opposite.

The neutral shift in the 180-day skew may be partly fueled by structured products that sell higher strike call options to generate additional yield alongside spot market holdings.

The rise in popularity of the covered call strategy could be lowering call implied volatility relative to puts.

Macro jitters

BTC dropped over 4% last week, nearing its previous record high of $11,965, as the core PCE, the Fed’s preferred inflation metric, increased in June. Meanwhile, disappointing nonfarm payroll figures raised concerns about the economy.

This price decline has led short-term skews to dip below zero, indicating traders are seeking downside protection through puts.

Ardern believes that the inflationary effects of “supply chain impulses” are already evident in economic data.

“While falling auto prices in the last CPI report counterbalanced rising prices for other goods, one fact is clear: the impulse from the West Coast has reached the East Coast, and retailers are attempting to pass on tariffs and associated costs to consumers. While wholesalers and commodity trading firms are working to alleviate supply chain issues, price increases will still happen, though possibly more modestly or ‘delayed by several months’,” Ardern explained, commenting on the renewed neutrality of long-term BTC options.

According to JPMorgan, President Donald Trump’s tariffs are likely to boost inflation in the latter half of the year.

“Global core inflation is expected to reach an annualized rate of 3.4% in the second half of 2025, primarily due to a tariff-related spike in the U.S.,” analysts at the investment bank noted, adding that cost pressures will likely be concentrated in the U.S.

An increase in inflation could complicate the Fed’s ability to reduce rates. Trump has consistently criticized the central bank for maintaining rates at 4.25%.

Traders are set to receive the ISM non-manufacturing PMI later Tuesday, providing insights into inflation in the service sector, a significant part of the U.S. economy. This will be followed by July CPI and PPI releases later in the week.

Read more: Bitcoin Still on Track for $140K This Year, But 2026 Will Be Painful: Elliott Wave Expert

Leave a Reply